The psychology of markets is not especially consistent. Investors get overly pessimistic when they are worried, and overly excited when newsflow is good. This creates periods where too much of the bad news is reflected in market prices and vice versa.

After 18 months of bad inflation and interest rate news, their view of the future was not a positive one. They’d just run a gruelling marathon, uphill, in the dark, at 2am in the morning. Some better inflation news was the energy drink they needed, and the reaction was euphorically quick, with a sprint to the finish into year end.

By the time we got to early January, expectations were for interest rates to be cut 5-6 times in 2024 (from 5.25% to 4% in the UK for example), and economies to remain resilient. To us, that felt unlikely. If economies are resilient, Central Banks would likely be cautious and reduce interest rates slowly, and if they were to reduce them quickly it would probably be because economies were weakening. Overall, although possible, a combination of solid growth and significantly lower interest rates felt a little bit like wishful thinking. We’d moved from overly pessimistic to overly optimistic, so within our portfolios we reduced a few of the positions that had performed so well in Q4 and built cash levels.

Data in January has continued to suggest that economies are slowing. At the same time market expectations that Central Bankers would support the view of early interest rate reductions diminished, causing equity and bond markets to have a healthy wobble in the first few weeks of the year. After such a strong Q4, a small correction in January was not really surprising, with bond and most equity markets selling off a little. Investors had started to appreciate the risks again, and with expectations more balanced, we reinvested our cash in areas where we have conviction. As markets improved into month end, we are hopeful that our activity this month will prove beneficial to returns down the line.

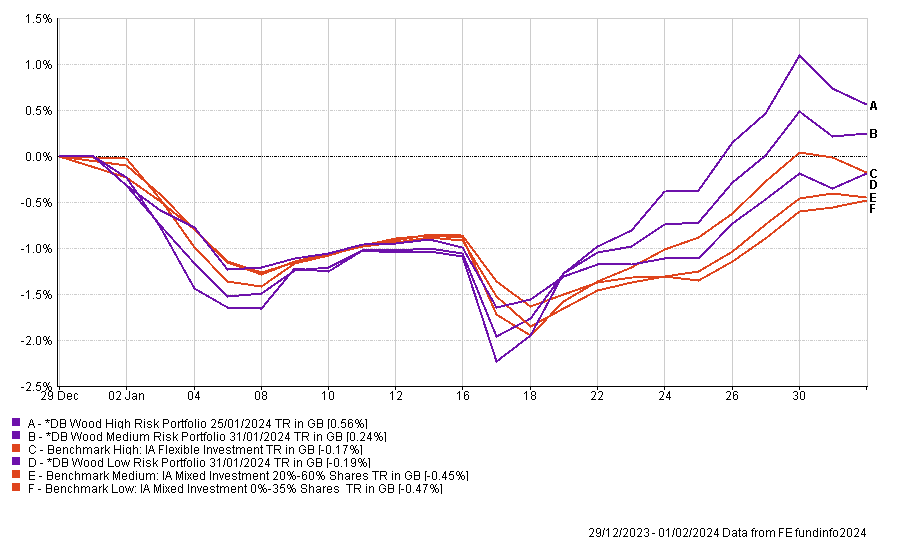

Overall, the portfolio range finished around flat in January, with returns between -0.26% (Very Low) and 0.53% (High). After finishing 2023 well ahead of benchmarks it was positive to see this trend continue into this year as well, with average outperformance of more than 0.5% in the first month of the year:

One month is not a long time to view things over, so in many respects this is a small part of the overall puzzle. That said, we hope it illustrates how we are managing our portfolios even based on short term market changes, all with the target of trying to steadily and consistently improve the results.

In our last quarterly update we highlighted that the first quarter was one that felt reasonably risky. The basis of that view is that by the time we get into the second quarter, inflation really will be close to 2%, allowing interest rates to start to come down. Even if they don’t come down 5-6 times this year, any movement is going to be positive for economies, so the chance of a recession reduces as the year wears on. We are just one month in, and although data hasn’t been brilliant, nothing has been out of the ordinary and expectations look a lot more measured than they were a month ago. So far so good.

This is a custom heading element.This is a custom heading element.This is a custom heading element.This is a custom heading element.

I am text block. Click edit button to change this text. Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elit tellus, luctus nec ullamcorper mattis, pulvinar dapibus leo. I am text block. Click edit button to change this text. Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elit tellus, luctus nec ullamcorper mattis, pulvinar dapibus leo. I am text block. Click edit button to change this text. Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elit tellus, luctus nec ullamcorper mattis, pulvinar dapibus leo.

I am text block. Click edit button to change this text. Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elit tellus, luctus nec ullamcorper mattis, pulvinar dapibus leo. I am text block. Click edit button to change this text. Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elit tellus, luctus nec ullamcorper mattis, pulvinar dapibus leo.

I am text block. Click edit button to change this text. Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elit tellus, luctus nec ullamcorper mattis, pulvinar dapibus leo. I am text block. Click edit button to change this text. Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elit tellus, luctus nec ullamcorper mattis, pulvinar dapibus leo. I am text block. Click edit button to change this text. Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elit tellus, luctus nec ullamcorper mattis, pulvinar dapibus leo.

OFFICE

Amber River DB Wood

Our team at Amber River DB Wood includes Chartered financial planners who look after clients across the East Midlands and beyond.

Join our mailing list

Small, but important print

We adhere to the FCA’s principles of Treating Customers Fairly (TCF). Read more here

Amber River DB Wood is a trading name of DB Wood Ltd, which is authorised and regulated by the Financial Conduct Authority no: 209530. Registered in England & Wales. Registration No. 4312250. Registered Address: Potterdyke House, 31-33 Lombard Street, Newark, Nottinghamshire NG24 1XG. http://www.fca.org.uk/register

The Financial Conduct Authority does not regulate National Savings or some forms of mortgage, tax planning, taxation and trust advice, offshore investments or school fees planning.

Please read our Privacy Statement before completing any enquiry form or before sending an email to us. You’ll find our Client Privacy Notice here.

For help if things go wrong click here