Bonds are a core component of our lower risk portfolios, so we thought it worthy of note, to try to explain the recent sell off, the implications for investing moving forward, and the effects on the wider economy.

This week we’ve seen another wave of political turmoil in the UK, something we have unfortunately become accustomed to in recent years. Given a 5 year election cycle, you would usually expect two Prime Minister’s every decade, but in the last 10 years we have already have 5, with a real prospect of a 6th on the horizon.

Political uncertainty doesn’t help anyone, other than maybe the two or three people vying for the next premier job. Investors in particular dislike the uncertainty. If you are sat in the US with billions of dollars to allocate globally, are you likely to allocate more or less to the UK this week? It is natural therefore, that we have seen weakness in all UK assets in recent days, but that is not a new thing, and is instead part of a consistent trend of money moving out of our market.

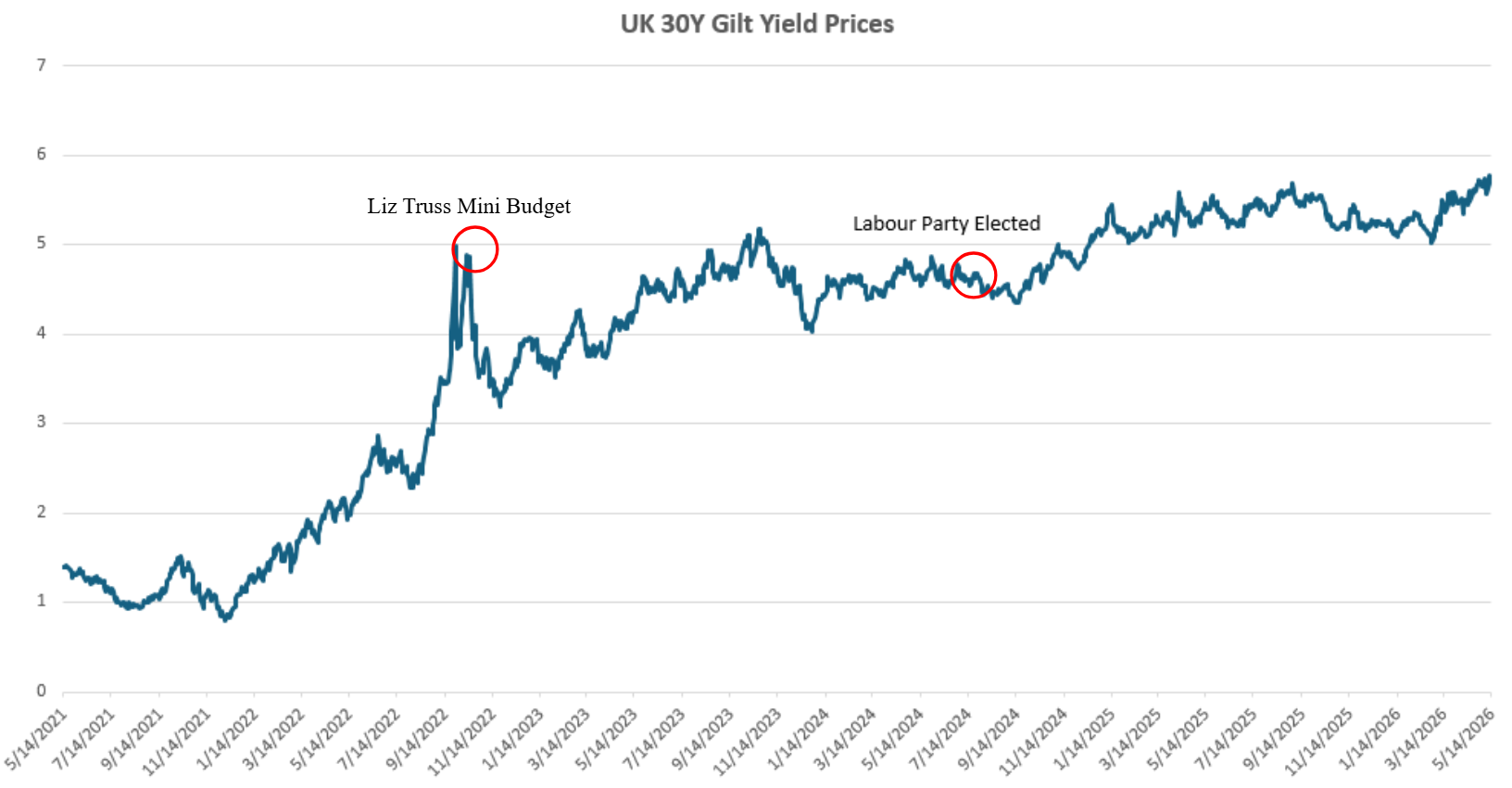

UK Government bond markets, as an example, are now approaching levels not seen since 1998. Bonds are a core component of our lower risk portfolios, so we thought it worthy of note, to try to explain the recent sell off, the implications for investing moving forward, and the effects on the wider economy.

With bonds, there is an inverse relationship between price and yield (income as a proportion of price). So as bonds sell off, the yield increases, and vice versa. Higher yields are better for future returns, as you then receive more income, but they also reflect market participants placing a higher degree of risk on the investment. Therefore, UK bonds are selling off faster than anywhere else in the G10, basically reflecting investors belief that the UK is now a riskier market. They therefore feel, they should be compensated more for owning UK Government versus say US Government bonds.

The core issue here is confidence. Bond investors care about one thing above all: will they get repaid in money that still holds its value? Right now, several things are making them nervous about the UK.

As an investment position today, the income available is highly attractive, with income returns available of 2-3% above the level of inflation, which is as good as we have ever seen it.

1. Political instability: Investors dislike uncertainty. Recent turmoil around Prime Minister Keir Starmer and fears of leadership changes have raised concerns that future governments could borrow more heavily or loosen fiscal discipline. Markets still remember Trussonomics in 2022, when gilt markets crashed after unfunded tax cuts were announced.

2. Government borrowing: A further increase in government debt beyond what is already factored in is a concern. Britain already runs large budget deficits and has a high debt load. Investors worry the government may need to issue huge amounts of new gilts for years. When supply rises faster than demand, bond prices fall and yields rise.

3. Inflation fears: Bond investors hate inflation because it erodes the real value of future interest payments. The UK is seen as especially vulnerable to energy-price shocks because it imports a lot of energy. Rising oil and gas prices linked to Middle East tensions have made investors think inflation could stay high for longer.

4. Higher interest rates for longer: If inflation stays high, the Bank of England may keep interest rates elevated. Existing bonds that were pricing in lower rates then become less attractive, so investors sell them.

5. Structural changes in the gilt market: For years, UK pension funds and the Bank of England were massive buyers of gilts. That support is weaker now, with the Bank of England selling bonds instead of buying them and pension funds also buying fewer gilts.

6. Weak long-term growth outlook: The UK has had sluggish productivity growth for years. Investors worry the economy may not grow fast enough to comfortably support rising debt levels. Slow growth plus high borrowing is a bad combination for bond markets. The UK’s comparatively high level of personal taxation means the environment is negative in terms of incentivising and encouraging growth.

To be clear, the above reasons do not mean that we think Britain will default like an emerging-market country in crisis. The UK can still print money in its own currency, has deep financial markets and a lot of history. However, investors increasingly want a “risk premium” (extra return) to lend to Britain compared with safer or more stable countries like Japan or Switzerland for example. Even Italian debt pays a full 1% less than the UK over 30 years!

What does this mean for investors and our lower risk portfolios? Positively, all the factors above now mean there’s so much bad news already priced in, and therefore we don’t think the sell off continues much further. As an investment position today, the income available is highly attractive, with income returns available of 2-3% above the level of inflation, which is as good as we have ever seen it.

If the political, inflation, and interest rate risks that are priced into valuations don’t materialise, we should see some very good capital appreciation in addition to the strong income. We therefore expect to start to see buyers come back into the market, particularly if Starmer survives into the summer, and there is an improvement in the Middle East conflict. Altogether, from this point forwards we expect to be able to generate returns of between 5% and 7% per annum from UK gilts, with a decent chance of an even better outcome if things head in the right direction. Low risk clients should therefore be comforted that despite all the news headlines, UK Government bonds today are very attractive in our view, and with a lot of bad news already priced in, the investment journey from here should be positive.

OFFICE

Amber River DB Wood

Our team at Amber River DB Wood includes Chartered financial planners who look after clients across the East Midlands and beyond.

Join our mailing list

Small, but important print

We adhere to the FCA’s principles of Treating Customers Fairly (TCF). Read more here

Amber River DB Wood is a trading name of DB Wood Ltd, which is authorised and regulated by the Financial Conduct Authority no: 209530. Registered in England & Wales. Registration No. 4312250. Registered Address: Potterdyke House, 31-33 Lombard Street, Newark, Nottinghamshire NG24 1XG. http://www.fca.org.uk/register

The Financial Conduct Authority does not regulate National Savings or some forms of mortgage, tax planning, taxation and trust advice, offshore investments or school fees planning.

Please read our Privacy Statement before completing any enquiry form or before sending an email to us. You’ll find our Client Privacy Notice here.

For help if things go wrong click here