Market Review

We entered the year with global equity valuations a little stretched. Inflation was on a downward trend and looked to be under control, economic growth was strong in the US and subdued though not recessionary elsewhere, and interest rates were coming down. Although there were pockets of weak economic data, such as rising unemployment in the US and the UK for example, there was enough good news to offset or allay any fears. For markets, the inflation and interest rate trends ruled, helping bond valuations to improve further and giving equity markets sufficient steam to move higher still.

Well, that was the story for the first two months of the year anyway. Our own FTSE 100 index led the pack moving into March, returning over 10%, UK Gilts (government bonds) added 2.5%, and most other markets also produced positive results, save the main US index (S&P 500), which lagged its global peers, only just managing to peer into positive territory.

So overall a great start to the year, with all our portfolios well ahead of their return targets through to the end of February. Then on the last day of that month, President Trump decided to take offensive action to disarm Iran’s nuclear program and in turn reduce their growing influence in the Middle East.

Overall, we would sum up the market in Q1 2026 as more volatile than expected, though at the same time more resilient than we would have feared given the circumstances.

Consequently, oil prices leapt to over $100 a barrel (from c$60) hitting their highest level since 2022, and the dollar strengthened as markets went into risk off mode. Just like when Russia invaded Ukraine, energy stocks suddenly became the cool kids again, leading Q1 equity flows, with most other sectors well in the red. Gold rose a bit further initially, though then dropped over 10% as investors rushed to liquidate positions to create cash.

The main shock to markets was the rapid rise in live energy pricing, not just in oil but natural gas as well. As prices rose, fears grew around a re-emergence of inflation, which in turn could lead to interest rate cuts being paused or worse, reversed. Both equity and bonds prefer lower interest rates and don’t like higher ones, so they both fell as forecasts for interest rate cuts were replaced with those for multiple increases. The UK equity market fell by over 6% in March, government bonds by over 4% and the US stock market by circa 3.5%. Now in isolation those seem like big moves, and they are, but in context of the gains of the last few years, currently we feel it is a modest correction.

Overall, we would sum up the market in Q1 2026 as more volatile than expected, though at the same time more resilient than we would have feared given the circumstances. Once again, we are reminded that diversification is absolutely key to protecting downside risks, and allowing a foundation for buying into valuation opportunities that emerge.

Portfolio Review

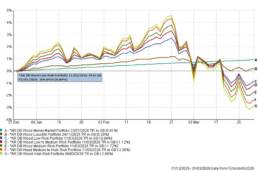

It is probably not a surprise that in March the portfolios lost all they had gained in the first two months of the year. Our lower risk portfolios out performed their benchmarks, with our higher risk portfolios slightly behind, having outperformed in 2025. Generally though, we are pleased with our portfolio returns given some of the repositioning that has been done during the quarter, which should bolster returns over the short, medium and longer term.

In this regard we have bought into some of the opportunities that we have been presented with given some very large sector valuation movements in March. The UK banking sector is a great example, which sold off very hard. It could be argued that higher interest rates would lead to better bank profits, provided we avoid a hard recession which we see as unlikely. We have therefore added to our banking allocation, as we feel that there is a significant opportunity for growth from here.

Fixed income (bond) markets also saw some huge moves, with bond yields moving out to levels, last seen in October 2023. Across just over two weeks, a 3 year UK government bond went from yielding 3.5% to 4.5%, a 28% increase. We have been adding steadily to our bond exposure as again we now see excellent value. If the war is prolonged, bonds should offer protection as growth starts to get pulled. If it is cut short, they will recover quickly. A win win scenario almost from here we feel.

Market Outlook

Our portfolio outlook is very dependent on how the war in Iran progresses. Sadly geopolitics has taken centre stage for our return outlook, from a backdrop which we felt remained supportive for our portfolios. To compare to 2022 for example, although this time we have seen a spike in gas prices, it has been nowhere near to one we saw when Russia entered Ukraine. Equally, we have as yet, not seen any spike in food prices. On the negative, the jobs market is weaker presently than in 2022. All this suggests to us that the interest rate rises that are priced into bond valuations are overdone, and this should mean we have more stability moving forward and more upside potential from this sector.

As our regular readers will know we are big on forward scenario and stress testing within our portfolios. To this end our central case would be for a stalemate of tensions with periodic escalation and de-escalation. Having said that, it feels like we revise our forecast almost daily dependent news flows, which is often unclear and ambiguous. A thirst for only acting on facts in terms of what we actually know remains difficult though paramount. Our outlook section this time around can only look at the value and opportunities we see, to run alongside the layers of protection we can add. To try to map forward based on a specific plan with any real conviction would be fool’s gold. A speedy resolution to the conflict (next 2-3 weeks) would be a big positive for markets, and a more prolonged situation would significantly increase the challenges.

There is not much support in the US for Trump's war, and the lack of engagement from some nations in support of the US is notable.

Notwithstanding that, our experience points us to look at picking up areas of value and quality when we see them. We have increased our exposure to quality short dated bonds, which are paying well above cash rates with both capital protection if things get worse and upside if the war were to draw to a close quickly. If the war is elongated we would likely consider adding also to long dated bonds, on the basis that a recession would then be more likely.

We have added equity risk in sectors that we think have sold off indiscriminately in March, and where we think there is very good long term value. Our preference is for value and quality in combination. For example, the UK banking sector is now trading on a 20% discount to where it was only one month ago. Similarly, we have reduced equity risk in sectors where we feel there is more downside risk than upside potential, such as India and emerging markets, though overall we continue to place emphasis on diversification.

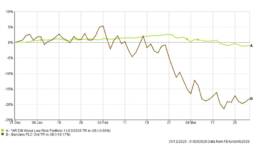

The chart below illustrates this well, looking at the share price movements of Barclays, one of our biggest UK equity holdings, against our low risk portfolio, which demonstrates the benefits of running a diverse portfolio. You can see that despite holding that stock, the portfolio has shown remarkable resilience. Particularly if the war is not prolonged, and/or a deep recession is avoided, then we expect to see a significant benefit from an increase in Barclays share price, and hence we now want more exposure. In fact, already since midday yesterday the stock is up 7%.

Of course, we would all love a resolution to the conflict. It doesn’t appear to be to anyone’s benefit if it were to become protracted. There is not much support in the US for Trump’s war, and the lack of engagement from some nations in support of the US is notable. It is therefore not beyond reasonable expectation that the war is brought to a premature conclusion in the near term. If that were to happen we would expect to see a quick recovery in equity markets and a rebound in fixed income returns. Regardless, we do expect the oil price to remain elevated (versus our expectations at the start of the year), and this will have a slightly more subdued effect on equity markets. Anything in the $70-85 range is very manageable, and equally, we expect that monetary stimulation that will follow through interest rate cuts should be supportive for both equities and bonds.

In the worst case scenario, equities are at further risk, though we would expect fixed income to become an anchor, as shorter dated government bonds would rally hard in that environment as economic growth expectations are revised down.

Of course we remain nimble and flexible. We have the ability to add cash at very short notice, and equally buy into other areas of opportunity should they continue to be presented. Rest assured, history has shown that it is impossible to time the depth of a market reaction, or when it might turn. What we do know is that it always does turn, and that you have to stay invested to reap benefits longer term. We certainly see no difference to our outlook from that regard.

Assuring you of our best attentions, and wishing you a restful Easter break.

OFFICE

Amber River DB Wood

Our team at Amber River DB Wood includes Chartered financial planners who look after clients across the East Midlands and beyond.

Join our mailing list

Small, but important print

We adhere to the FCA’s principles of Treating Customers Fairly (TCF). Read more here

Amber River DB Wood is a trading name of DB Wood Ltd, which is authorised and regulated by the Financial Conduct Authority no: 209530. Registered in England & Wales. Registration No. 4312250. Registered Address: Potterdyke House, 31-33 Lombard Street, Newark, Nottinghamshire NG24 1XG. http://www.fca.org.uk/register

The Financial Conduct Authority does not regulate National Savings or some forms of mortgage, tax planning, taxation and trust advice, offshore investments or school fees planning.

Please read our Privacy Statement before completing any enquiry form or before sending an email to us. You’ll find our Client Privacy Notice here.

For help if things go wrong click here