Written by:

Alex Chappell

Investment Manager at Amber River DB Wood

Market Review

Investment markets were somewhat erratic over the last three months. As we have now become accustomed to, Trump played a major role, though equally renewed conflict in the Middle East was also a significant contributor.

Even before anyone had managed to use this year’s ISA allowance on 6th April, markets were in freefall, struggling to understand the policy direction of the US administration, which had ramped up tariffs on all economies. In the days that followed, things got worse before they got better, specifically between the US and China who got stuck in an escalatory spiral which at one stage left the effective tariff rate on any goods travelling from China to the US at 145%.

Let’s all take a second to say thanks to the bond market, which played a key role in Trump rowing back his policy stance. Between April 2nd and April 11th, bond yields (government borrowing rates) had moved up about 0.5%. This doesn’t seem like much, but when you think of it in terms of mortgage rates and business loans, it is significant. Willingness to lend then naturally dries up, making life very difficult, particularly for those with debt obligations that need to be put into place or refinanced. Any sharp move in bond yields can therefore cause the whole financial sector to grind to a halt. This time round, the contraction in financial conditions was happening at the same time as good shipments had fallen off a cliff due to the high tariffs in place. We therefore spent most of the start to the quarter staring down the barrel of an approaching recession. Trump thankfully calmed everything as quickly as he escalated it, a turn of events that would later be dubbed the ‘TACO’ trade, standing for ‘Trump Always Chickens Out’. Dare you to say that to him at a press conference. This is also a good example of the investment markets controlling political decisions that it perceives as risky or challenging. A similar market response occurred in the UK leading to the demise of Liz Truss in October 2022.

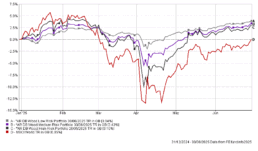

After April 11th equity and bond markets recovered, and at the time of writing they are more or less where they were at the end of Q1. If you’d have looked at your portfolio on 1st April and not looked again until 1st July, you would have thought it would have been a reasonably stable period, though as the chart below shows, the journey has been volatile with global stocks falling nearly 20% from their peak in Q1 to their bottom in Q2.

*For reference, the MSCI World is a commonly used benchmark for the performance of Global Equities, and IA UK Gilts the same for UK Government Bonds.

On the economic data front things were understandably mixed. Given the news on tariffs, there was a lot of forward orders to avoid the anticipated price hikes that tariffs might bring. This increased imports, which helped to drag US GDP into the negative for Q1. Importantly though, even when you take out the anomalies, it suggested a slowdown in US growth. Jobs data in the quarter looked fragile as well, with fewer new jobs being created, and internally, US air flights reduced markedly, further making the case that activity is reducing. On the other side of the equation though, the corporate environment has remained robust, with corporate profits looking solid. This data is slightly more retrospective, so doesn’t tell the whole story yet, but it challenged the otherwise disappointing data set.

Similarly, there were mixed results in the UK, with economic activity picking up through the first 4-5 months of the year, but with some big questions remaining. Retail sales, as an example, came in at -2.7% for May, the biggest monthly decline in two years, with comparable results in other European economies. The market’s perception of the UK government is not great, and as a result the UK’s cost of borrowing has risen, due to a lack of confidence in the Labour administration ability to improve the UK’s fiscal position. They have such a large majority but the administration appears to lack cohesion and a togetherness as well as a credible plan to deliver growth. This is keeping bond yields high, which is a good thing for investors longer term, though this is not an enabler for UK investment. The government needs borrowing costs to fall, in order to use the debt interest savings to invest in economic growth.

It would also be remiss not to mention ongoing geopolitical tensions as a key factor in Q2. There was certainly a time in the quarter where there looked to be progress towards peace in both Ukraine and Gaza. Neither of course materialised, and in addition we now have wider Middle East conflict to factor in.

For markets the biggest knock-on has been volatility in commodity prices, with oil down overall on the quarter, but having rallied by 10% in either direction on a few occasions. Gold has been a big beneficiary, both of geopolitics and the trade drama. In fact since the start of 2025 the yellow metal is up 25%, reaching an all-time high in April. Related to that has been a fall in the US dollar, as we sit today £1 buys $1.37, up from $1.29 on the first of April. In the portfolio context this is also key, as any US dollar assets have lost significant value due to the currency movements over the quarter.

So there has been lots to unpack. Overall markets are positive over three months, albeit the journey has been volatile especially through April. Heading into the rest of the year we are assessing various forward pathways, which remains challenging given the distortions in economic data. We expand upon this in our market outlook with the expectation that as we go through Q3 things will get clearer. Fingers crossed!

Portfolio Review

As an investment team, we are always very focused on providing diversification. Anyone can place a big bet on one asset class or theme and get lucky, but it takes good judgement and understanding to provide consistent performance in a variety of environments. In order to do so, you have to make sure you own things that perform well at different times. By spreading your allocations, and finding things that complement each other, you both reduce risk and improve consistency. We think fanatically about this, also reflective that our biggest past mistakes have happened when we are too concentrated. Valuable lessons that have helped develop and reinforce our philosophy.

I make that point because the market environment is now one that is much more suited to a diversified approach. In the zero interest rate decade, US equities and in particular US technology provided super-charged returns, and relative performance was primarily about how much you invested in that one theme. Since interest rates have ‘normalised’ things have changed, with many more factors now at play, suiting a diversified approach over one that is concentrated.

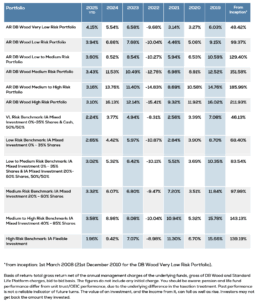

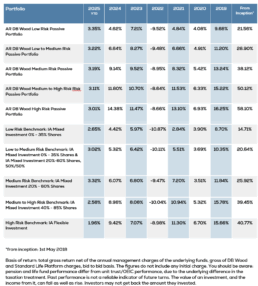

Zooming in on this quarter, the portfolios delivered returns of between 2.57% (Very Low) and 5.25% (High Risk). This leaves year-to-date returns between 3.10% (High Risk) and 4.15% (Very Low Risk) at the halfway stage, once again well ahead of our respective benchmarks.

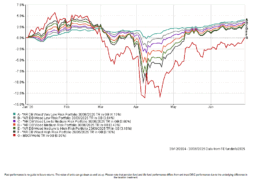

One point to make here is that the lower risk portfolios are naturally more diversified than the higher risk ones. They have greater allocations to bonds, alternatives and cash, whereas the higher risk portfolios have a greater concentration in equities. The fact that they have performed better this year so far is thanks to that added diversification, which ensured they held up better in the periods of volatility, making it easier to bounce back when things recovered. You can see this clearly in the chart below, comparing all six risk profiles across the period:

Even within our equity allocation we are constantly searching for diversification. One example that has helped us this quarter is our overweight position to the UK and Europe, which have continued to outperform the US. It may also be of interest to know that where we do have our US equity allocation, around 30% of it is hedged. This has taken the negative currency effects out of the equation and for UK investors made a material difference to returns. Our hedged US equity position is up 11% on the quarter, compared to the unhedged at 5%. Again, these positions were taken with diversification in mind, aiming to reduce the reliance of the portfolios on our asset class or currency.

From a positioning perspective, we finished quarter one explaining that we had reduced risk across the first few months of the year and were positioned cautiously, having built some cash positions. As I’m sure you’ll expect, given the volatility in April, we were busy deploying some of our cash before taking profits again in May, but again we finish the quarter cautiously positioned. Part of this is down to the lack of conviction in the growth outlook, though another reason is the amount of good ideas we have across different asset classes currently. With our fixed income bucket still offering around 6% per annum, and our alternatives bucket on track to deliver that type of net return with low levels of risk as well, we do not need to chase one particular area to deliver strong returns moving forwards, nor are we overly reliant on growth to achieve our clients objectives.

Market Outlook

The market consensus currently is that there will not be a recession in 2025. This is built on the idea that trade deals will be done, corporates and consumers will continue to weather the storm, and higher levels of government spending twinned with progressively lower interest rates, will help to stimulate growth. That consensus is the key reason that equity markets have been able to recover from April so strongly, so the main question from here is will that outlook materialise in the second half of the year?

The short answer is we don’t know. There are certainly reason to believe it could, though also lots of reasons to believe it won’t! Being positive, despite the looming 90-day trade deadline, there are still lots of possibilities that might arise, such as the deadline extending. Moreover, given the fact that Trump’s policy focus has shifted towards the ‘Big Beautiful Bill’ (BBB), it is likely that the worst of the trade war is over. On the other hand, the longer that uncertainty lasts, the worse it is for corporates who have a greater inclination to hold off making big decisions.

Touching on fiscal spending as the second market assumption, in the UK we are learning the hard way how difficult it is to raise spending when you have government debt at these levels. What Trump is proposing is one of the biggest increases to their debt ceiling in history, at a time where bond markets are already very worried about the sustainability of the debt. In this respect it feels like there is a lot of hope… equity markets hoping it gets passed to help prevent a recession, and bond markets hoping it gets blocked to stop the debt spiral. Someone is going to be disappointed, both of which would have negative economic consequences.

The one positive we do agree on is the interest rate trajectory. Despite inflation being temporarily higher here in the UK, generally speaking it continues to be close to target globally. Moreover, we continue to move through the integration of AI into the workforce, which even if you are sceptical about its ability in a general sense, it will make things quicker, easier, and therefore cheaper (reducing inflation), as well as driving more profit, leading to more investment and more economic growth. On the other hand, if economies worsen, Central Banks should then have the headroom to keep lowering interest rates. Either way our portfolios should be able to navigate to positive returns.

The upshot of all of that is that we can see a number of different potential outcomes ahead. There is one where deals are done and Trumps beautiful bill is passed, which would have one set of implications for bonds and equities. Then there is another where the deal gets blocked and the trade uncertainty causes further economic weakness, which would have a completely opposite set of effects.

It won’t surprise you that our stance is therefore to be cautious and diversified. In this respect our equity allocation remains high quality, spread across all geographies without a huge bias. Our bond allocation is shorter in duration (term/ length) at 4-5 years, which reduces the sensitivity to big swings in interest rates and meaning income yield (5-6% per annum) remains the biggest driver of returns. Finally, our alternatives position, which includes cash, is also the biggest it has been for two years. Here we have a number of unique exposures which should be able to deliver between 5% and 8% per annum which a low correlation to equities and bonds.

All together we are positive that the portfolios are positioned to perform in a variety of forward environments. By Q4, we expect to know a lot more about which one is most likely, giving us the chance to adjust things accordingly.

OFFICE

Amber River DB Wood

Our team at Amber River DB Wood includes Chartered financial planners who look after clients across the East Midlands and beyond.

Join our mailing list

Small, but important print

We adhere to the FCA’s principles of Treating Customers Fairly (TCF). Read more here

Amber River DB Wood is a trading name of DB Wood Ltd, which is authorised and regulated by the Financial Conduct Authority no: 209530. Registered in England & Wales. Registration No. 4312250. Registered Address: Potterdyke House, 31-33 Lombard Street, Newark, Nottinghamshire NG24 1XG. http://www.fca.org.uk/register

The Financial Conduct Authority does not regulate National Savings or some forms of mortgage, tax planning, taxation and trust advice, offshore investments or school fees planning.

Please read our Privacy Statement before completing any enquiry form or before sending an email to us. You’ll find our Client Privacy Notice here.

For help if things go wrong click here