Market Review

Q3 was positive for most risk assets, with several markets, notably gold and Global equities all moving higher. Tariff policy continued to fade into the background, with fiscal and monetary easing helping to provide markets with positive sentiment. The combination of large fiscal deficits and lower interest rates is a positive tailwind for risk assets. These are both known to boost economic growth, therefore reducing the chance of a recession. To summarise, US policy has shifted from being anti-growth and spending in Q1, to pro-growth and spending since.

In our last update we wrote about the challenges in interpreting current economic data. We felt that economies were looking challenged, and additional costs via tariffs might add further pressures to growth. In Q3 markets seemed less concerned about the tariff story, taking the view that companies and the consumer were well placed to deal with price rises. In addition, headline GDP figures have been solid (even in the UK we seem to be tracking well), and company earnings in general have been ahead of expectations. In contrast though, labour markets in most developed economies are showing signs of a slowdown. Job hires in the US have averaged 27k per month in the last four months, compared to a total of 122k in the first four months of the year.

Moreover, wage growth in the US, Europe and UK continues to slow, and graduate hiring is at cycle lows. The housing market is also very slow in the UK, and this is so often a barometer for consumer confidence.

Government debt levels are a core reason why the gold price pushed through its all-time high

At the same time, inflation has been sticky. The UK rate is now at 3.8%, up 0.4% over the quarter and sitting at the worst level in the G7. That said other areas such as the US (2.9%), and Europe (2.4%) have also seen increases across the quarter, with recent data releases generally suggesting a lingering inflation picture irrespective of region.

Global equity markets also produced very good returns after a very volatile 2nd Quarter. Increasing expectations for Central Banks to cut interest rates also helped equities and bonds to perform well over the quarter. The Bloomberg Global Aggregate Index produced 2.35% over the quarter, a very solid outcome for a typically lower risk asset class.

That said, bond performance by region differed significantly, with the UK in particular underperforming due to higher inflation and budget speculation. As we touched on in our Question the Committee blog two weeks ago, the UK 30 year bond now offers an income yield of 5.5% per annum. Comparatively it was 5.2% on July 1st, and 4.6% this time a year ago, a trend that suggests investors have significant concerns about the management of the UK’s fiscal position.

Government debt levels are a core reason why the gold price pushed through its all-time high. The growth in tandem of gold and many global stock markets is unusual, generally it is an asset class that performs well when other markets struggle.

Altogether it was an interesting quarter for financial markets. Equity markets shrugged off mixed economic data to perform well, and bonds liked the prospects of further interest rate cuts. The overriding factor here was tariff noise abating and supportive policy coming through, though the latter raised further questions around fiscal sustainability, shifting prices in longer duration bonds and certain commodities as well.

Portfolio Review

When positioning our portfolios we always try to picture a number of forward scenarios. This helps us not only to position for what we think is most likely, but also to consider the risks and opportunities in our outlook.

Coming into the last quarter there was significant divergence in our scenarios, largely due to the uncertainty lingering from the first quarter. In this respect we were not yet sure how the tariff noise would show in the underlying growth and inflation data, so although market valuations were attractive in many areas, we still approached it with caution and emphasised diversification across the portfolio range.

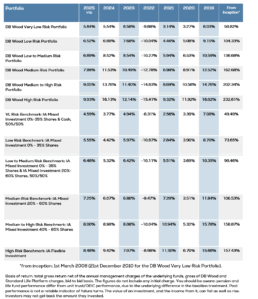

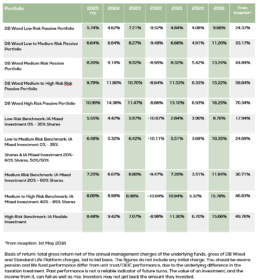

From a positioning standpoint, all year we have emphasised diversification. This has helped us perform consistently across the period, with all portfolios underpinned by strong income yields of 3% (High Risk) to 6% (Very Low Risk).

At the same time, it is important to acknowledge that we are now in a regime where interest rates sit above the level of inflation. That may seem like a normal thing to say, but historically it hasn’t been the case for most of the last 15 years. The key implication is that even by holding lower risk assets such as shorter duration bonds, you are able to lock in a solid return (2-3% per annum) above inflation. As an example, our bond allocation has returned over 6% in the last 6 months, with very low levels of volatility.

That said, as the quarter progressed, we became more comfortable that the policy landscape was more supportive (in the short term), and therefore we gradually added more equity risk back into the portfolios, taking profit on some of our bond holdings which had performed well. This has helped provide a strong outcome with portfolios overall returning between 1.62% (Very Low Risk) and 6.63% (High Risk) over Q3. When added to the first two quarters, the portfolios are looking well set with just three months of the year left, all ahead of their respective benchmarks.

From a positioning standpoint, all year we have emphasised diversification. This has helped us perform consistently across the period, with all portfolios underpinned by strong income yields of 3% (High Risk) to 6% (Very Low Risk). We haven’t got every decision right (in hindsight we would have added to equities aggressively in April), but it has felt like a period where a lot of risks have been navigated, and so to have

delivered strong portfolio outcomes across the board despite a more cautious stance is pleasing.

Market Outlook

The final quarter of the year is usually an interesting one, and we expect no different this year with a number of key questions remaining. The starting point is that markets now expect a very positive trajectory, especially in the US. ‘The government will keep spending, interest rates will keep coming down, and economic growth will be ok’ is now the base case, though we see a number of challenges to that outlook. There is lots of good news priced into markets, and therefore we would suggest caution at this point, particularly if interest rates don’t come down as quicky as anticipated, the jobs market continues to cool and inflation remains stubborn.

Interest rates could come down more quickly if economic data deteriorates, but that would naturally be a bad thing for equities, and it would also make the government fiscal position worse as tax receipts fall. The price of gold is already telling us that government balances need to be better controlled, and that means they also need economic growth to be solid. If growth is solid, then there is a risk inflation keeps bumbling in the background, meaning interest rates can’t be reduced as quickly.

All of those factors are therefore interconnected, and the outlook is different by region. Given a higher inflation picture in the UK, the Bank of England is now not expected to cut interest rates further before year end. We actually expect inflation to subside reasonably quickly here in the UK – a pull back into the 2s over the next 6 months seems reasonable – which could allow more aggressive easing here, and a bit of positive help for the Chancellor around The Budget.

Investment markets, particularly in the US have a lot of positive news priced into them, and therefore we see the US outlook as too rose-tinted, and the UK as too pessimistic. Accordingly, we remain underweight US assets, and overweight UK assets, both in equities and bonds. Maybe this time is different…

Despite some caution over current market expectations, we also agree that the chance of a global recession is now lower as Trump has moderated his tariff stance. If growth were to slow further, then we would expect inflation to move with it, therefore giving Central Banks room to cut interest rates and stop a worse situation developing. This is one of the key reasons we have been happy to selectively add equity exposure in the last quarter, as the worst-case scenarios have become less likely.

Overall our positioning has slightly changed over the last quarter, but generally speaking our outlook is the same. We are fully invested, with low cash levels, but continue to hold a preference for diversification by asset class, region and investment style. Income yields remain strong, helping to underpin returns, and giving us a strong baseline from which to continue to deliver good returns over the months and years ahead. That said, we do enter the fourth quarter with positive market expectations, especially in the US, and hence we will remain nimble, hoping to use any market volatility to our advantage.

OFFICE

Amber River DB Wood

Our team at Amber River DB Wood includes Chartered financial planners who look after clients across the East Midlands and beyond.

Join our mailing list

Small, but important print

We adhere to the FCA’s principles of Treating Customers Fairly (TCF). Read more here

Amber River DB Wood is a trading name of DB Wood Ltd, which is authorised and regulated by the Financial Conduct Authority no: 209530. Registered in England & Wales. Registration No. 4312250. Registered Address: Potterdyke House, 31-33 Lombard Street, Newark, Nottinghamshire NG24 1XG. http://www.fca.org.uk/register

The Financial Conduct Authority does not regulate National Savings or some forms of mortgage, tax planning, taxation and trust advice, offshore investments or school fees planning.

Please read our Privacy Statement before completing any enquiry form or before sending an email to us. You’ll find our Client Privacy Notice here.

For help if things go wrong click here