Written by:

The Investment Committee

Market Review

The positive momentum for risk assets continued through the fourth quarter, albeit with increased volatility. Overall, this completed a strong year for equity markets, supported further into year end as expectations for interest rate cuts increased heading into 2026. The combination of reducing interest rates and large government deficits has caused recessionary fears to fade into the background, leading investors to be more risk-on as we look forward to 2026.

In terms of numbers, global equities (proxied by MSCI All Countries World Index) added just over 3% in Q4. The divergence between geographies was significant though, with the US market adding 2%, and the main UK index, despite dropping 5% in one week in November, adding 7% on the quarter, benefiting from its large index weights to banks and miners.

Despite the positive sentiment, economic data has remained mixed. The labour market in most major economies continues to slow, with job openings and wage growth trending down and unemployment rates steadily ticking up. These are usually not good signs, but it is worth highlighting that most developed economies are still near full employment, so these negative trends do come from a very solid base. In addition, in certain economies such as the US, immigration restrictions have had a significant effect, meaning that a decent chunk of the weakness is down to policy change rather than actual economics.

Bond markets have enjoyed the improving inflation trends, and as such also had a good fourth quarter.

Labour market jitters have also been overshadowed by spending and investment, in particular by the AI hyperscalers (Google, Nvidia, Meta etc), who continue to invest at historically strong rates. This spend is, of course, more of a US centric phenomena, but as the worlds largest economy, it is a key one for markets. With inflation slowing, along with jobs and wage data, investors could see a better environment for more borrowing, so in this sense, the micro outcomes of a few mega stocks have been a key factor dictating the macro outcome for global economies.

When looking for evidence to support the positivity going into the close of 2025, inflation trends across the developed world have been good in Q4, with data releases coming in lower than expected. UK inflation is a good example of this, with the rate falling from 3.8% in September to 3.2% in November.

Bond markets have enjoyed the improving inflation trends, and as such also had a good fourth quarter. Our fixed income allocation which includes UK Gilts, US Treasuries and a wide variety of corporate bonds, added 2% in Q4, not far off global equity returns, though without the volatile journey, which was an outcome we hoped for.

Finally, to finish the round up it is worth mentioning gold, which again has had a lot of newsflow having made new all-time highs in recent months. Similar to equity markets, it has benefitted from expectations of further interest rate cuts and government spending (larger deficits are usually good for gold), though additionally a key driver has been geopolitical uncertainty. The world continues to be a tense environment with issues looming around Venezuela, Greenland, Taiwan, the Middle East, Thailand, not to mention Russia, China and the US.

Portfolio Review

We came into the fourth quarter positively positioned – fully invested with low cash positions. However, we remained cautious that markets were too optimistic in outlook, giving little consideration to the key risks. At the same time some of those risks had become less likely, and as such we wanted to take advantage in areas where we felt most convicted.

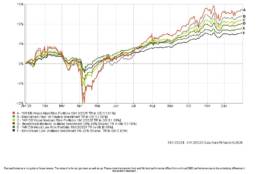

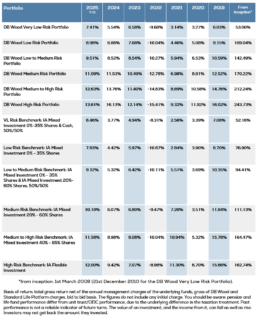

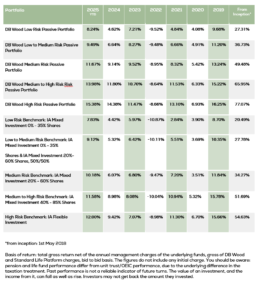

As you would expect then, the portfolios performed well. The main range added between 1.47% (Very Low Risk) and 3.34% (High Risk) over the quarter.

It is quite unusual for both our bond and equity allocations to have a strong quarter together. At the most basic level, they are both owned to diversify each other, though there are times where they move in the same direction, such as over the last three months. In addition, with respect to equities, we specifically benefitted from having an overweight position to the UK and Europe, which were the two leading markets in Q4. Similarly in bonds, our positions felt the benefit as economic conditions suggested interest rates might reduce further. Not only were the markets good, but our allocations within those markets preferable, which is always pleasing.

Investors enter 2026 in a buoyant mood. The oil price is now 50% lower than it was 3 years ago, and inflation levels are expected to fall allowing room for interest rates to follow suit.

Being critical, the main decision we didn’t get right in Q4 was our allocation to gold and other precious metals, which is low. Gold is currently a highly volatile asset class, with the fundamentals for growth difficult to call. A reduction in geopolitical tension would likely prove negative, and with Trump on the hunt for an end to the Russia Ukraine conflict, we have kept exposure low here. Peace hasn’t materialised, and other conflicts and stresses have appeared. This is not a basis for investment that we feel comfortable with. Of course, geopolitics is not the only driver of the gold price, though this year it has been heavily shaped by it.

Outside of that though it was another strong quarter for returns, capping another strong year and building on the numbers delivered in 2023 and 2024. Will 2026 be the fourth consecutive year of above target portfolio returns… only time will tell, but we will do our best to map it out in our outlook next.

Market Outlook

Investors enter 2026 in a buoyant mood. The oil price is now 50% lower than it was 3 years ago, and inflation levels are expected to fall allowing room for interest rates to follow suit. The chances of a US led recession now seems very remote, and therefore the economic climate in the US which seems pro investment and consumer suggests that 2026 could be another good year for stock market returns.

Similarly, bonds should do well in this environment. Without a recession, corporate bonds should remain in demand, and with the capital expenditure supported by lower interest rates, then supply should be there to meet that demand. Although yields have reduced a little on 12 months ago (we have seen some capital appreciation in bond values so the yields have fallen as a result), future bond returns should be close to the level of income currently received (c4-5%), in addition to further capital growth, giving a return expectation of 6-7% pa from low risk assets, assuming our central case plays out.

The key question then, is what could go wrong? There are probably two main tail risk events to consider here.

The first, is that just at a time where no one is talking about a recession, we actually have one (when we talk about ‘one’ we are really talking about a US/global recession, not a technical recession in the UK which is a lot more conceivable – just less important to global markets). How could this happen? Well with the labour market already weakening, we would argue that economies are reasonably vulnerable to any kind of significant shock. Perhaps some of the tech businesses that are spending heavily on AI will start to scale that investment back, which in turn would cause a significant market correction and loss of confidence. That in itself could be enough to cause a recession.

How likely is that in the next 12 months? We would say unlikely, but it isn’t a 0% probability either, and so any time investors are acting like it is, it is worth taking note.

The second risk is quite the opposite, which we could term the “run it too hot” scenario. As you may or may not have seen, President Trump has been putting a lot of pressure on the Federal Reserve to cut interest rates. In this respect it is worth remembering that cutting interest rates is stimulative, so you only really want to do that when you really need it. The US President has the power to select his own Federal Reserve Chair, with the swap due to happen in May this year. Should he select someone who is not ‘independent’ and in turn the Federal Reserve start aggressively cutting interest rates at a time where US growth is already strong, then we could easily see higher inflation return to accompany higher growth. At the same time, there would be a loss of confidence in the US monetary system, which would have significant consequences.

Is this one likely? Some market commentators certainly think so, but we would say not. There are a few points here but in short, although the Federal Reserve Chair has power, he only has one vote, and needs a majority to cut interest rates. Secondly, the mid term elections are in November, so there is a lack of time and benefit to making a policy error to help a President who is likely to be constrained from then onwards.

Either way, it is interesting to map out the possibilities, and consider where the current consensus could be wrong. If it isn’t, and things keep playing out positively, then we are well positioned to benefit and deliver another year of strong returns. If not, then we would need to pivot quickly, and so a lot of time and effort has and will continue to go into planning for those alternative worlds. For now, all is good, but 2026 is likely to be a year where volatility is high and you need to stay nimble. Thankfully, that’s exactly the type of environment our team works well in.

OFFICE

Amber River DB Wood

Our team at Amber River DB Wood includes Chartered financial planners who look after clients across the East Midlands and beyond.

Join our mailing list

Small, but important print

We adhere to the FCA’s principles of Treating Customers Fairly (TCF). Read more here

Amber River DB Wood is a trading name of DB Wood Ltd, which is authorised and regulated by the Financial Conduct Authority no: 209530. Registered in England & Wales. Registration No. 4312250. Registered Address: Potterdyke House, 31-33 Lombard Street, Newark, Nottinghamshire NG24 1XG. http://www.fca.org.uk/register

The Financial Conduct Authority does not regulate National Savings or some forms of mortgage, tax planning, taxation and trust advice, offshore investments or school fees planning.

Please read our Privacy Statement before completing any enquiry form or before sending an email to us. You’ll find our Client Privacy Notice here.

For help if things go wrong click here