Market Review

We entered the quarter, one month in from start of the US and Iran conflict, following which oil had spiked from c$70 per barrel to well over $100, and there was the very real possibility that the conflict would spread across the Middle East.

Thankfully, what followed was a two-week ceasefire announced on 8th April, followed by a number of extensions before the formalised 60-day truce was announced in mid-June. Markets reacted at different paces to the news, with equities bouncing back strongly from the end of March onwards, effectively announcing the conflict was over before the announcements were made. In contrast, both oil and bond markets were a little more conservative, finally starting to rally back from early June.

Part of the reason equities were so resilient was thanks to a very strong company profits being reported out of the US. The tech sector almost to a company beat earnings estimates, signalling positive things to come thanks to the record demand for computing power. Usually this would lead to a market where returns are unproportionately driven by a narrow set of stocks, though on this occasion the benefits were broader, with both European and emerging market tech sectors also performing strongly, as well as a number of other areas of equity markets including small-caps and financials.

From an economic perspective, one key outcome of the war is a temporary upward push on inflation. At the start of this year we had expected UK inflation to fall back towards 2% by now, though as we sit today we still have an annual rate of 2.8%. This is likely to persist over the next few months until fuel prices come down, before it starts falling again into 2027. Interest rates have, therefore, been held and markets expect them to hold current levels for the rest of this year at the very least. The picture is very much the same in the US and Europe as well. So in short, whilst inflation is contained, we know it is stickier than we expected prior to the conflict.

It is of course pleasing that our central case on Iran played out, and since that point the portfolios have performed extremely well.

Another area we have commented on in recent updates is gold and precious metals, which performed very strongly in 2025 and at the start of this year. Q2 however saw a big correction across these markets, with Gold down more than 10% and Silver and others seeing further weakness. The challenge for these markets has been the ‘higher for longer’ interest rate narrative, which makes non-yielding assets less attractive relative to bonds for example.

Finally, it would be remiss not to finish the review without talking about the changes in the UK political backdrop over the last quarter. In this regard we’ve seen the resignation of Sir Kier Starmer, and the rise of his likely successor Andy Burnham through the Makerfield by-election. For UK assets like gilts, the pound, and domestic equities, the policy landscape from here will be a key determinant of returns, and to that end we will add more flavour to what we expect in our outlook.

For now, it has been a strong quarter for financial markets, with both bonds and equities benefiting from a de-escalation in the Middle East, a fall in oil prices and strong company reporting. That leaves us halfway through 2026 in positive territory, which when added to the positive returns delivered in 2023, 2024 and 2025 leaves us in a position where it feels hard to remember the last time markets were difficult for an extended period, albeit there have been some geopolitical curve balls along the way.

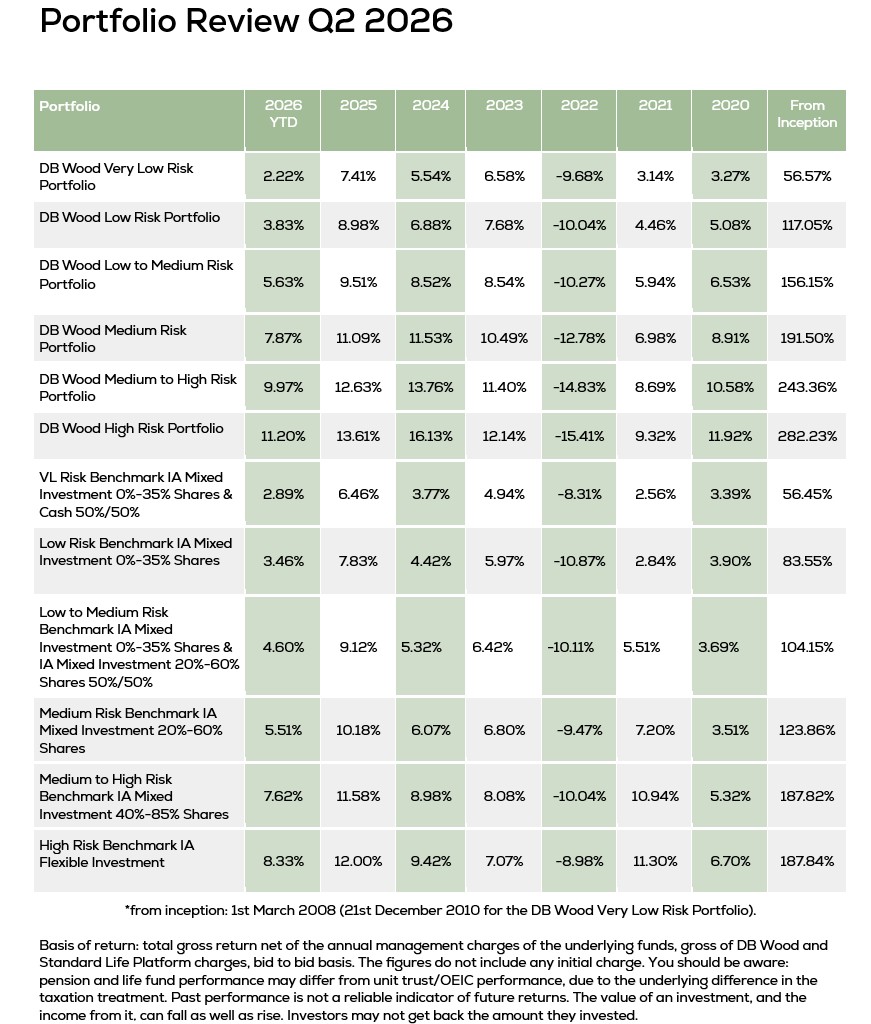

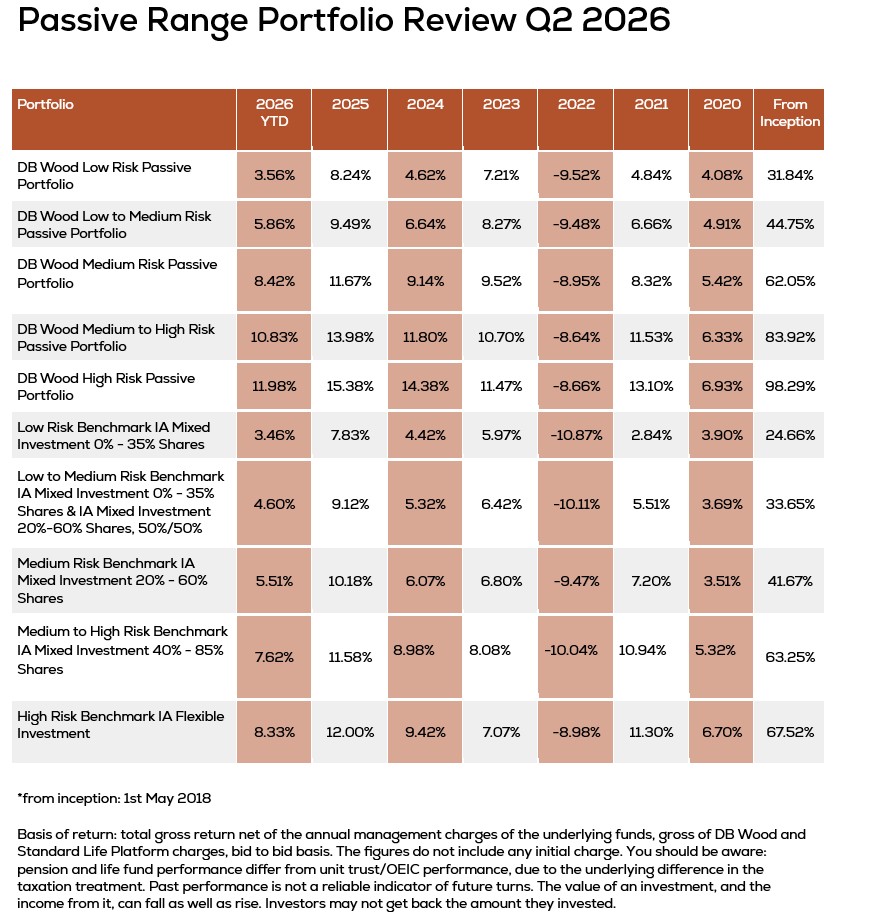

Portfolio Review

Whenever we approach our investment opportunity set, we always try to build multiple scenarios of how things could play out. Our objective is not to bet everything on one path but instead find a balance, that will ensure the portfolios perform well in multiple regimes, tilting our exposures to the scenario we feel is most likely.

As regular readers of our blogs will know, we consistently held a more positive view on the Iran conflict, certainly when compared to the financial and political media which to a man seemed convinced this would be Russia-Ukraine v2. Again, that isn’t to say we didn’t have hedges in place, as we needed to be sure that if we were wrong, clients capital would be protected, but at times it did become an anti-consensus view that things would be solved in a matter of months.

All the evidence to us suggested it was in no-ones interest to let this continue for long enough to let it become a real economic problem, and that allowed us to gradually buy assets at cheaper valuations as the conflict worsened. We did this both in equities and bonds, the latter of which saw yields move out to levels above what we saw in Liss Truss’ 2022 mini-budget.

At one point the UK 30-year bond yield hit 5.9%, effectively meaning you could buy that bond and lock in 5.9% for 30 years. When you consider that long term equity returns are around 7% per annum, that is quite incredible relative value. Similarly, a UK 3 year Government Bond moved from 3.5% per annum to 4.6% per annum in just a few weeks, reflected market expectations that the Bank of England would have to hike rates given the pending inflation surprise. We didn’t believe that was likely, and even if it happened, we had a high level of income locked in, so it felt like a good risk-reward across a number of scenarios. We added around 5% to our bond allocation across that period, with an average return since those purchases of c3% over the quarter.

This example once again reflects what it means to be active managers, which can be a significant benefit in periods of high volatility, as markets provide opportunities for those that can look through the short-term noise.

It is of course pleasing that our central case on Iran played out, and since that point the portfolios have performed extremely well. But it isn’t always the case that we get everything right, and it is important to not get carried away by one month, quarter of year in isolation. Our job is to make improvements to client returns over time, and deliver a journey they can rely on and feel confident in when times are difficult.

Market Outlook

The macroeconomic backdrop remains supportive for financial markets. A combination of good economic growth, especially out of the US, inflation that should now trend back towards 2% into 2027 and interest rates which still have room to come down, are all positive tailwinds to returns. Despite three and a half good years in a row, there is every chance that over the next 6-12 months markets continue to grind up and delivery positive outcomes.

A lot has also been made about a potential ‘bubble’ in the AI supply chain, which in our view is the biggest risk to the current momentum changing. There are still big questions about whether the level of spend the hyperscalers (Google, Amazon, Microsoft) will be justified in hindsight, but they are the worlds most profitable companies, and as long as they continue to spend then all the people they are spending with will continue to benefit. We’ve seen share price growth across a much broader part of the tech universe over the last quarter, and our base case remains that this continues until one of the big guys blink.

At the same time it is important to note that when that blink does happen, it will be a significant market risk. It would have the exact opposite effect of the continual increases in spending commitments that we have seen, and could single handedly cause a US and therefore likely global recession. The bubble may well burst eventually then, and we would therefore have to be quick to react if this scenario played out. It should be pointed out that we are very light on technology exposure in our lower risk portfolios. Generally clients views here remain more about capital preservation combined with a solid return above inflation, than delivering high returns by maintaining positions in what are undoubtably expensive assets.

At the same time, geopolitical risks remain high, though with Trump about to move his focus to the mid-term elections, and the US-China relationship seemingly more amenable after his state visit, it feels like the risks are lower than they have been for some time. Iran could twist and turn over the next 60 days, but it still feels like the most likely outcome is a long term agreement.

Interestingly every round England qualify for in the World Cup is estimated to add 0.1% to GDP, so here is to cheering for more heroics on Saturday night – if nothing else, do it for the economy boys!

On the US mid-terms, it is highly likely that the house moves across to the Democrats, which would then erode the Republican control of both parts of the US political system. This is a very normal process and is more likely than not if history is to be repeated, making it harder for a standing President to enact policy as easily. Interestingly the third year of a US election cycle is usually the best for equity markets, and we may well therefore see a more sanguine Trump in the second half of this term (if that is possible!).

In the UK we expect Andy Burnham to replace Sir Kier Starmer as the 7th UK Prime Minister in 10 years. He will inherit many of the same challenges, albeit we can see a window of opportunity where if he is sensible in his initial policy changes, and he strikes a tone of stability and balance, then we could start to get some economic momentum. Over the last three years savings rates in the UK have hit all-time highs, with savers having put to one side £50-60 billion per annum (JO Hambro, 2026). If inflation falls back towards 2% as we expect in early 2027, and the Bank of England gradually loosen interest rates further, then maybe some of these savings will start to unlock and the economy get going again. Maybe that is us being too optimistic, but it is an environment that would be good for both UK equities and bonds, of which we have a good allocation to both.

We have focused a lot on the US and UK as two core regions, but there remain opportunities across Europe, Emerging Markets and Japan too. Similarly, the bond story is not just about UK politics, but a high income yield that will continue to delivery 3-5% per annum depending on the portfolio range even if nothing changes.

All together the outlook is positive. As always, it is not without its risks, and we will continue to carefully map out a number of scenarios and pivot quickly if it is required. The portfolio range remains diversified, but it is positioned positively for now. With interest rates close to 4%, if the main risks are avoided, then returns should be nicely in excess of that even at the lower end of the portfolio risk range.

A lot will happen across the next quarter, not least in the UK political landscape. Interestingly every round England qualify for in the World Cup is estimated to add 0.1% to GDP, so here is to cheering for more heroics on Saturday night – if nothing else, do it for the economy boys!

OFFICE

Amber River DB Wood

Our team at Amber River DB Wood includes Chartered financial planners who look after clients across the East Midlands and beyond.

Join our mailing list

Small, but important print

We adhere to the FCA’s principles of Treating Customers Fairly (TCF). Read more here

Amber River DB Wood is a trading name of DB Wood Ltd, which is authorised and regulated by the Financial Conduct Authority no: 209530. Registered in England & Wales. Registration No. 4312250. Registered Address: Potterdyke House, 31-33 Lombard Street, Newark, Nottinghamshire NG24 1XG. http://www.fca.org.uk/register

The Financial Conduct Authority does not regulate National Savings or some forms of mortgage, tax planning, taxation and trust advice, offshore investments or school fees planning.

Please read our Privacy Statement before completing any enquiry form or before sending an email to us. You’ll find our Client Privacy Notice here.

For help if things go wrong click here