In business, it’s often said that “cash is king”, but it doesn’t rule in every realm. When saving for your long-term goals, it could be investments that deserve the crown.

Cash is useful for your easy-access emergency fund or short-term savings, but data shows that it’s less likely to outpace inflation than investments over the long run, even with the additional risk that comes with investing.

So, if you’re saving for 10, 20, or 30 years down the road, investments may be a better option. Read on to learn why holding too much cash could harm your long-term wealth goals.

Inflation can erode the value of your cash savings

Cash savings can provide guaranteed returns, so you may think that it’s a safe way to build wealth for your future. However, if your cash returns are lower than the rate of inflation, your money will lose value in real terms over time.

When inflation is higher than saving rates, price rises will chip away at the spending power of your cash, and your savings could lose substantial value in the long run.

Let’s say inflation averaged 5% over a 12-month period. That means goods and services that cost you £1,000 at the start of the year would cost you £1,050 at the end of it.

If you put £1,000 in an easy-access savings account at the start of that year, paying 3% interest, you’d have earned £1,030 interest over the same period. So, you’d effectively have “lost” £20 in real terms.

Recently, in the 12 months to May and June 2024, the rate of inflation dipped to 2% – that’s below the Bank of England’s (BoE) base rate of 5.00%.

According to Moneyfacts, many providers currently offer savings accounts with rates above 2%. So, in the current economic climate, cash savings could provide returns that outstrip inflation.

However, as the below graph shows, inflation has been higher than interest rates for most of the last four and a half years:

Source: Financial Times

Additionally, with inflation at target levels, many forecasters expect the bank to cut the base rate again soon.

When this happens, it might not be long before you see banks and building societies reducing their saving rates. So, even though saving rates currently outstrip inflation, this could soon change.

As a result, to give your wealth the best chance of beating inflation as you work towards your long-term goals, it’s sensible to consider investing your money.

Indeed, data from Unbiased reveals that, in the last 10 years, the average return on Stocks and Shares ISAs has been 9.64% annually, versus 1.21% for lower-risk Cash ISAs.

Investing could give you a better chance of outpacing inflation

Though cash may not be best for building wealth in the long run, it can have its place in your portfolio. It can be useful for:

- Your emergency fund

- Saving for short-term goals (less than five years away)

- Reducing risk in your pension fund as you approach retirement

- Balancing risk in your portfolio

Meanwhile, when saving for longer-term goals, investing could give you a better chance of beating inflation and generating a better return on your money.

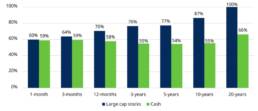

The chart below shows your chances of beating inflation when holding either cash or investments (in the form of large cap stocks) over several years:

Source: Schroders

As you can see, no matter how long you hold them, cash savings have a 54% to 66% chance of beating inflation.

Conversely, the longer you hold investments, the greater your chance of beating inflation. And, as illustrated, holding investments for 20 years leads to a 100% chance of outpacing its eroding effects.

A diverse investment portfolio could help to protect and grow your wealth

Of course, while investing your money can give you a greater chance of beating inflation and give you the potential for a better return, there’s always a possibility your holdings could fall in value.

However, the right mix of cash and other asset types like equities and bonds can help to limit the risk in your portfolio, an approach known as “diversification”.

Diversification spreads your money across different asset classes, sectors and geographical regions. While it won’t remove all risk from your portfolio, when one of your investments falls in value, another might rise, and this can help to smooth the returns on your money.

Building a portfolio that strikes the right balance between investments and cash, and that reflects the level of risk you’re comfortable with and can afford to take, should give you the potential for growth over the medium to long term.

When investing your money, an Amber River financial planner will design an investment strategy that ensures you hold a diverse range of assets, giving you the greatest chance of generating the growth you need as you work towards your financial goals.

They can also advise you on how much cash you should hold to meet short-term goals and provide a safety net in the event of an emergency, without harming the potential to grow your wealth in the long term.

Get in touch

To discover how an Amber River planner could help you build the right portfolio for you, call us on 0800 915 0000, or alternatively use our contact form here to set up an initial appointment.

Disclaimer

The information within this article was correct at the time of publishing, but laws and tax rules are subject to change. Your circumstances and where you live in the UK may also have an impact on your tax treatment.

To learn about the government’s most recently-announced changes, please read our latest budget roundup: 2024 Autumn Budget Update