The gap between generations is widening, and not just when it comes to technology, culture, or fashion. Our children today face a very different retirement landscape from the one we are preparing for.

The state pension, once the cornerstone of retirement income, is under growing strain. With rising life expectancy, an ageing population, and the costly “triple lock” promise, governments are spending more than ever to maintain state pension levels.

By the time our children retire, the state pension may look very different. It could be means-tested, start much later, or offer a lower level of support. That’s why many parents and grandparents are asking what they can do now to help their children, and grandchildren, when they get older.

The State Pension challenge

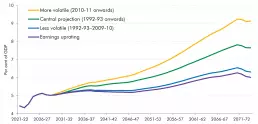

Government figures show that state pension spending is rising faster than the economy can comfortably sustain. The Office for Budget Responsibility (OBR) projects that expenditure will increase from around 5 per cent of GDP in 2024–25 to nearly 8 per cent by the early 2070s. More than half of this increase will be driven by the triple lock, which guarantees that pensions rise by the highest of earnings growth, inflation, or 2.5 per cent each year.

State pension spending under different triple lock scenarios

Source: DWP, ONS, OBR

While this promise has been welcomed by today’s retirees, it comes at a cost. The OBR has warned that if the triple lock remains in place without other reforms, public debt could rise to unsustainable levels.

To balance the books, governments may have no choice but to change how, and to whom, the state pension is paid. With the state pension age already rising to 67 by 2028 and to 68 in the mid-2040s, some experts believe future generations could be waiting until 70 or even 75 before they receive support.

The barriers facing young people today

Even if the state pension does survive in its current form, young people face their own challenges in building a retirement pot. The cost of living remains the biggest barrier. House prices are still high, energy bills have increased, and according to the government’s own statistics, the average graduate leaves university with more than £53,000 of student debt.

For many, saving for something that’s 50 years away feels unrealistic when they are focused on getting on the property ladder or paying for childcare.

Employment patterns are also changing. Younger generations are more likely to work in the gig economy or switch jobs regularly, which can disrupt workplace pension contributions and lead to gaps in pension savings.

Awareness is another issue: research by M&G suggests that many young people underestimate the savings required to achieve even a moderate retirement income, meaning they risk undersaving for decades.

With the state pension age already rising, some experts believe future generations could be waiting until 70 or even 75 before they receive support.

How you can help your children save into a pension

One of the most powerful ways parents and grandparents can make a difference is by contributing to a pension on your child’s behalf.

A Junior SIPP or stakeholder pension allows contributions of up to £2,880 (2025/26 tax year) each year, which is automatically topped up to £3,600 thanks to basic-rate tax relief, even if your child has no earnings.

Starting early could have a significant impact thanks to the power of compounding. Money invested when your child is young has more time to grow and recover from market fluctuations. Even relatively small contributions made over many years could build into a meaningful retirement pot by the time your child reaches their 50s or 60s.

Education is just as important as financial support. When your child starts work, explain how their workplace pension and auto-enrolment work, and encourage them not to opt out. Even a modest contribution, combined with employer payments and tax relief, can put your child on track to a healthier retirement income.

Easing the financial burden so your children can save

Not every parent will feel comfortable locking money away until their child reaches retirement age. Another way to help is to reduce some of the financial pressures they face today, so they have more freedom to save for themselves.

- Education support: Contributing to university costs can reduce student loan balances and help your children begin their working lives with more disposable income.

- Housing help: Whether it’s gifting a deposit, offering an interest-free loan, or acting as a guarantor, supporting your children with their first home can free them from years of high rent and allow them to save sooner.

- Childcare costs: According to the Coram Childcare Survey 2024, the average cost of full-time nursery care is now over £14,000 a year. Helping with these expenses, or even providing practical childcare, can relieve pressure on household finances.

- Lifetime gifting: Using the annual gifting allowance (£3,000 per person) or making larger gifts that fall outside the estate after 7 years can be a tax-efficient way to transfer wealth.

- Avoiding deprivation of assets: It’s vital to ensure gifts are affordable. If they are made deliberately to avoid paying for future care, local authorities may challenge them.

Estate planning considerations

Inheritance Tax (IHT) receipts have reached record highs in recent years, partly because the nil-rate band of £325,000 has been frozen since 2009. Without careful planning, more families than ever risk paying a significant tax bill that could erode what you pass on to your children.

Parents should review their wills regularly, make use of the residence nil-rate band where available, and explore the use of trusts or family investment companies where appropriate. A clear estate plan allows families to give financial support during their lifetime and pass wealth on efficiently when the time comes, helping to close the pension gap for the next generation.

Teaching your children financial literacy

Financial support is valuable, but financial education may be just as important. Teaching your children about the basics of saving, investing, and tax can build confidence and encourage good habits that last a lifetime.

Show your children how ISAs and pensions work, encourage them to save regularly, and discuss the importance of balancing short-term spending with long-term planning. These conversations can help your children avoid costly mistakes and take ownership of their financial future.

The role of professional advice

Pensions, gifting rules, and estate planning can be complex, and mistakes may be expensive. Working with a professional financial planner can help ensure that your family’s wealth is structured efficiently, gifts are made tax-efficiently, and retirement savings are invested appropriately.

For parents who want to support their children without jeopardising their own security, tailored advice can make the difference between good intentions and a sustainable plan.

Get in touch

Every family’s situation is different, and the right approach depends on your goals, assets, and comfort level. Our advisers can help you create a plan that balances your own retirement needs with the support you’d like to give your children, whether that’s opening a pension, gifting money, or structuring your estate.

To speak to an Amber River financial planner, call 0800 915 0000. Alternatively, you can use our contact form to arrange an appointment.

Disclaimer

The information within this article was correct at the time of publishing, but laws and tax rules are subject to change. Your circumstances and where you live in the UK may also have an impact on your tax treatment.