Article written by:

James Curry

Chartered Financial Planner

With over a decade of experience in financial services, James is both a Chartered Planner and an accredited SOLLA adviser, specialising in later-life planning, inheritance tax, and care funding.

I’ve had countless conversations with people about their workplace pension, and one thing stands out: the assumption that the default investment option is automatically the best choice.

After all, if it’s been set up by the employer and recommended by the provider, it must be designed to work for everyone, right?

In 2012 the government made it mandatory for most employers to provide their staff with a pension. This has resulted in over 10 million people now regularly saving into a workplace pension, many of whom hadn’t done so before. Generally, this is considered a policy success as it has helped the public make better provision for their retirement.

While workplace pensions have been a fantastic step forward in helping people save for retirement, the way they’re typically invested may not always be aligned with your long-term goals.

Over 10 million people now regularly saving into a workplace pension

How Workplace Pensions and Default Funds work

One of the most common strategies used is called “Lifestyling” or “Target Date” investing. It’s designed to gradually shift your pension investments from higher-growth assets to lower-risk ones as you approach your selected retirement date.

On the surface, this makes sense. But what if your actual retirement plans don’t fit neatly into this model?

Many people today are working beyond their planned retirement date, phasing into retirement gradually, or choosing to keep their pensions invested for longer. While others are opting to retire earlier than expected, whether that’s due to a change in circumstances, a career shift, or simply wanting to enjoy more free time.

In both of these scenarios, automatically shifting to lower-risk investments at the wrong time – whether too soon or too late – could impact your financial future. Retiring earlier than planned might mean your pension hasn’t had enough time to grow, while delaying retirement could leave your savings in overly-cautious investments that don’t keep up with inflation. Either way, ensuring your pension strategy aligns with your actual plans can make a big difference in how much you have to enjoy later in life.

In this article, I’ll walk through how Lifestyling funds work, the assumptions they rely on, and why it’s worth checking whether your pension investments are working in your best interests.

What are Lifestyling pension funds?

Lifestyling funds are designed to align your pension investments with your expected retirement date. For example, if you plan to retire at 60, the fund initially takes on more risk by investing in higher-growth assets, such as equities, since you have time to ride out market fluctuations.

As you get closer to retirement, the fund automatically shifts to lower-risk investments, gradually moving your money into a mix of cash and bonds, to reduce volatility and protect against market downturns.

On the surface, this approach seems sensible. However, it relies on two key assumptions that may not always hold true.

Assumption 1:

Lifestyling funds assume you will actually stop work on the date you selected when you joined your workplace pension, and that you keep the scheme updated with information about when you plan to retire.

Given 90% of people leave their pensions in the default option, I suspect that most won’t give that planned retirement date much further thought – or keep the scheme details updated as their life changes.

Assumption 2:

Prior to the Pension Freedoms Act in 2016, most of us were forced to use our pension pots to buy an annuity on retirement. This is a financial product that converts your pension savings into a guaranteed income for the rest of your life. For many people, annuities were, and still are, the most suitable option, but with Pension Freedoms came greater choice in how we take our pensions.

For instance, we can now take money from our pensions in lump sums, as and when we need them, or as a regular withdrawal, like you would from a bank account. This flexibility means you might choose not to buy an annuity, but keep your pension pot invested for years or even decades after your chosen retirement date.

The problem with Lifestyling funds

The logic behind Lifestyling funds reducing the risk of the portfolio as you near retirement is based on the link between annuity and bond prices. By gradually shifting more of your pension into bonds, the aim is to protect against fluctuations in interest rates, ensuring a smoother transition if you plan to buy an annuity.

This approach makes sense – if you’re going to buy an annuity. However, in 2023, fewer than half of retirees chose this option. They either left their pensions untouched or opted for a drawdown strategy instead.

If you’re among those who opt not to buy an annuity, the shift into lower-risk investments could work against you. A portfolio heavily weighted in bonds may struggle to keep pace with inflation, let alone generate the long-term returns needed to support your retirement.

When working with clients on their retirement plan, we’ll typically assume they will live to 100, as around 1 in 8 people already do (a number that continues to rise). Even if you don’t reach that milestone, this assumption provides a useful financial buffer. With that in mind, if you’re not buying an annuity, your pension could remain invested for 30 years or more after you stop working. This makes it crucial to ensure your investment strategy reflects this reality.

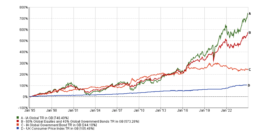

The impact over 30 years

The chart below illustrates the growth of four portfolios over 30 years:

- A – 100% global equity portfolio (this represents a higher risk portfolio typical of what a younger person in a Lifestyling fund would hold)

- B – 60% equity/ 40% bond portfolio (to represent a medium-risk portfolio.)

- C – 100% global bond portfolio (to represent the portfolio you are likely to hold once you reach the pension’s normal retirement date.)

- D – Inflation, measured as the Consumer Price Index (CPI)

An important point to note here is that none of the figures below include the effect of charges on your portfolio:

While the global bond portfolio has outperformed inflation over this period (before charges) and maintained its buying power, it has lagged behind a portfolio better suited for long-term investment. That gap could be the difference between enjoying the lifestyle you have in mind – whether that’s travelling, supporting your children / grandchildren, or simply having greater financial freedom – or having to scale back your plans.

Align your pension with your long-term strategy

This is why it’s essential to ensure your pension’s investment strategy aligns with your long-term life plans and overall financial goals. If you have any questions on this, or know anyone who may be affected, I encourage you to contact an independent financial planner – they will be happy to help.

Secure Your Retirement with Expert Pension Planning

Planning for retirement can be complex, but with expert guidance, you can ensure financial security for the future. Whether you’re looking to consolidate pensions, maximise tax relief, or understand your options, we’re here to help.

Speak to an Expert Today

Arrange a Callback

Fill in the enquiry form, and a member of our team will call you back to arrange a meeting.

Arrange a callback

Disclaimer

The information within this article was correct at the time of publishing, but laws and tax rules are subject to change. Your circumstances and where you live in the UK may also have an impact on your tax treatment.